Disclaimer: this is NOT investment advice, etc.

Introduction

Say you buy some BTC, ETH, DOGE, and watch the price go up and down along with your portfolio value. This is still traditional investing: holding these tokens in your crypto wallet or exchange is similar to owning shares of equities like AAPL and TSLA in your brokerage account. In simple words: the value of the asset position will fluctuate with the market, but the size of the position (number of tokens or shares) will remain the same.

This is the beauty of “Yield Farming”: processes that guarantee an increase in the quantity of committed assets, most commonly measured as Annual Percentage Yield (APY). Using the metaphor the name lends itself to: Yield Farming is the practice of growing various crypto-crops by sowing, harvesting, compounding, and rebalancing resources over time.

The first question I hear from folks with a healthy skepticism is: cryptocurrencies don’t photosynthesize, so where do these additional tokens come from? How can a token auto-magically multiply in my wallet, but still retain (and possible increase) its dollar value?

I love answering this question because it gets to the heart of what many see as the future of crypto: Proof-of-Stake (PoS) and Decentralized Finance (DeFi).

Contents

Section 1: Single-Token Farms

- Node Delegation

- Stablecoin Holding

- Decentralized Lending

- CrowdFunding Incentives

- Membership Rewards

- Reflection Tokens

Section 2: Token-Pair Farms

- Liquidity Mining

- Concentrated Liquidity

- Yield Aggregators

Section 3: Advanced Topics:

- Sustainable Farming

- Leveraged Farming

Node Delegation

Instead of solving Bitcoin’s complex mathematical equations as “Proof-of-Work”, the Proof-of-Stake (PoS) architecture allows any asset owner to delegate their tokens to a remote blockchain host. These staked tokens help the node validate transactions, which is what powers all blockchain networks.

To illustrate PoS, consider a blockchain-native video streaming platform. Theta Network (THETA) is a “decentralized peer-to-peer network that can offer improved video delivery at lower costs” according to the founder. It’s basically YouTube on blockchain, which is no coincidence since Steve Chen co-founded both companies. Enterprise Validators (including Google, Sony, and Samsung) and Guardian Nodes (user managed infrastructure) process transactions to ensure network stability, incentivized by TFUEL rewards.

And in order to process transactions, they need a whole lot of THETA! This is how anybody can support the network without having to maintain their own infrastructure: by staking tokens to a remote node. [Note: Edge nodes allow users to share their bandwidth in return for TFUEL, but do not validate blockchain transactions.]

PoS allows anyone to participate in a blockchain network and earn a portion of gas fees required for transactions, without having to set up all the equipment required to run a node. As a result it is also far more eco-friendly, which should be a a priority for anybody interested in farming.

Ethereum is due for a 2.0 upgrade (ETH2) which completely shifts from mining to PoS. But in the meantime, new blockchains such as Solana (SOL) and Polygon (MATIC) have come up with their own solutions. See this dashboard that shows Solana’s “validator” nodes with all tokens “delegated” from other holders. The following screenshot is the Staking dashboard for Polygon (MATIC):

Rewards from node staking are not straightforward to estimate. Polygon and others provide a calculator applet that allows you to tweak parameters such as staking duration and % of token supply locked, all of which impact the rate of rate of rewards at any given time. In essence, it doesn’t make much sense to say “staking MATIC will earn you _% APY”. So if you believe in and/or are bullish on a PoS asset, consider delegating to a node to earn some extra tokens and support the network.

Stablecoin Holding

Stablecoins are a special type of token whose price is pegged to a designated crypto or fiat currency. Each coin implements this using different financial mechanisms, but most are reputable and well-regulated: there is about $30B USDC in circulation at the time of writing, which is backed by $30B USD in a regularly audited fiat bank account managed by leading crypto companies including Coinbase and Circle. Though the predictable nature of stablecoins is ideal for daily use, we cannot actually purchase much with them yet.

So when you “buy” a stablecoin, this is not really an investment since you know upfront that the price will not change. This stability gave me personally the confidence to convert larger amounts from my fiat bank account into a reliable crypto asset, and enables a wide variety of transactions that will come up in the course of this article. To extend the botanical analogy, stablecoins are like synthetic plastic plants with very minor variations over time.

Holding USDC (and other stablecoins including USDT, DAI, gUSD, bUSD, sUSD, cUSD, MIM, etc.) contributes to the stability of its price, which is why most issuing platforms reward users for simply owning and not selling. Coinbase offers 4% interest on USDC deposits, Binance offers almost 3% on bUSD stakes, and I have seen as high as a 12% on platforms such as Nexo. Compare this to the fraction of <1% offered by most fiat banking institutions.

Coinbase, Binance, Gemini and other exchanges guarantee a 1:1 swap from stablecoin to fiat, so one could easily convert it today or 10 years from now to the same dollar value and withdraw to any fiat bank account. For no-risk and low-but-higher-than-fiat interest rates, consider converting some idle cash into stablecoins.

Decentralized Lending

According to Coinbase: “DeFi is an umbrella term for peer-to-peer financial services on public blockchains”, in other words a reimagining of our global financial systems without centralized banks operated by humans under government jurisdiction. The timeless example here is a secure, anonymous credit market where users can instantly get a loan without an institutional middleman.

Aave, which describes itself as “a non-custodial liquidity protocol for earning interest on deposits and borrowing assets”, is the earliest and most established player in this space. Earning passive income is only a few clicks away…

Where does your deposit go? Why are they rewarding you with free tokens? Is it safe?

Say you deposit 100 DAI (stablecoin worth $1) for which Aave guarantees you a 2.74% APY. Now I decide to borrow your 100 DAI coins at a higher interest rate of 11.94% APY.

So out of the 11.94% interest I pay Aave, they pay you 2.74% and use the remaining 9.2% towards revenue and other parts of the platform via smart contracts. Note that all loans must be collateralized: I must already have 100 DAI coins to prevent me from defaulting on the loan and stealing your coins. So yes, Aave is safe.

This “Open Source Liquidity Protocol” that supports reliable lending and borrowing with no human intervention (“permissionless”) inspired several similar services competing for market share. This financial model of pocketing the margins between borrowers and lenders is not specific to DeFi, in fact Fixed Income markets are entirely based on trading interest-bearing debt bonds. The huge innovation here is that any individual can participate as a creditor or borrower without requiring custom financial instruments or institutional gateways.

If you plan on holding relatively long term, you can safely earn high interest on a wide variety assets by depositing them into Aave or other reputable lending protocols.

CrowdFunding

In the summer of 2020 while most of the world was under lockdown due to the pandemic, DeFi really broke out with the Compound (COMP) Liquidity Mining program. It’s all very new but there are already some well funded and established players such as Aave, Curve, and Balancer. These are just a few of the many early-stage startups working to develop a variety of Web3 services, experiences, and worthwhile ways to spend your crypto including gaming, betting, curated datasets, paywall content, virtual reality, digital art, lots more on the way.

And of course, all startups need to somehow fund their ventures. There are several traditional ways to do this such as Venture Capital angel investments and Shark Tank style equity or credit deals (digression: Mark Cuban invested in Polygon/Matic). Then platforms such as Kickstarter and GoFundMe ushered in the crowdfunding model, which has become increasingly popular as it incentivizes early customers/investors/advocates to commit to the future of the project.

DeFi took this concept of early stage crowdfunding and to a whole new level. In order to gain traction and active users, which is ultimately what determines the financial value of any company, DeFi startups offer incentives to early adopters who financially endorse the project by “staking” tokens. The APYs on these staking contracts are particularly appealing in the early days, similar to how pre-construction homes are often sold at significant discount. Since the users’ tokens are locked in a smart contract, they cannot be sold or “dumped” which would lower the tokens price and market cap.

Staking also contributes to the Total Value Locked (TVL), the net value of all tokens held in a platforms’ smart contracts. This is one of the most important metrics as highlighted by DeFiPulse, and helps win the confidence of additional users and investors. The goal is to create a recursive, viral, network effect that will rapidly attract new users to the product, increase the tokens market cap, and boost the reputation of the company.

With this in mind, most DeFi startups allocate a portion of initial tokens towards user incentives. These “Tokenomics” charts clearly indicate allocations made towards user incentives, strategic partnerships, development, charity, scheduled burn, and other purposes. Initial allocations are crucial in determining the purpose and priorities of the business. Let’s take a look at Polygon (MATIC) vs. SolFarm (TULIP):

Comparing Polygon’s modest 12% rewards allocation to SolFarm’s relatively high 48%; we might deduce that the Polygon team envisions more use cases for its native token, while SolFarm plans to dole out rewards and could be more lucrative in the short term. On the other hand, Polygon’s 4x ratio between tokens allocated to development team (16%) and to advisors (4%) might inspire a bit more investor confidence compared to SolFarm’s 10x ratio with a 20% team and 2% advisor split.

These comparisons are solely to illustrate how we can analyze a tokenomics chart as it relate to crowdfunding and the business model. I think SolFarm is an excellent startup whose main product is innovative yield farming, so the 48% liquidity mining rewards makes sense in that context. We will return to it later to discuss advanced farming techniques.

Below are some example single-token staking pools that are easy to get started with. These companies have worked out a business model where they can offer you a certain % rewards for staking tokens. More fundamentally, these startup teams believe in themselves and their ability to sustain future growth.

- Harvest Finance iFARM: 25% APY

- Pancake Swap CAKE Syrup Pools: >90% APY AutoCompounding

Be careful with entering fixed-duration contracts: they are far riskier and thus rewarded with higher % than those where the user can unstake their funds at any time. I personally entered a fixed-duration 90 day staking contract for the Origin Token (OGN) with 12.5% annualized rewards. On May 1st 2021 just before the most recent crash the price was $1.82 , and when the contract finished on July 31st the price was $0.81. I ended up with about 3% more tokens and a 55% loss…but a 100% gain in knowledge and experience!

Membership Rewards

As pioneered by Compound, governance tokens provide powerful decentralized governance mechanisms. Decentralized Autonomous Organizations (DAOs) are a hugely important part of DeFi, but for now let’s stay focused on yield.

Some platforms offer users the privilege to metaphorically move from the casino table to the house. By “minting” non-fungible governance tokens (ie. purchasing membership), users are entitled to a small share of the platforms revenue. For trading platforms, more precisely Decentralized Exchanged DEXs which we discuss soon, this usually means users can have a small cut of trading fees. Here are 2 examples I am quite invested in:

- vDODO: “a non-transferable token that serves as a user’s proof of membership in DODO’s loyalty program”. Benefits include dividends from trading fees, reward tokens, and the steep 9% exit fee from members who cash out.

- xSUSHI: mint xSushi token which entitles you to “0.05% of all swaps on all chains”.

As we see with vDODO these membership tokens are often illiquid “wrapped” positions, and converting back to tradeable tokens can be expensive. Analogously if you purchase a year-long gym membership and want to cancel 5 months in, you probably won’t get the full 7 months back. So you should only consider this option if you really believe in the platform long-term, and may be willing to wait for the full year’s worth of APY before withdrawing your funds.

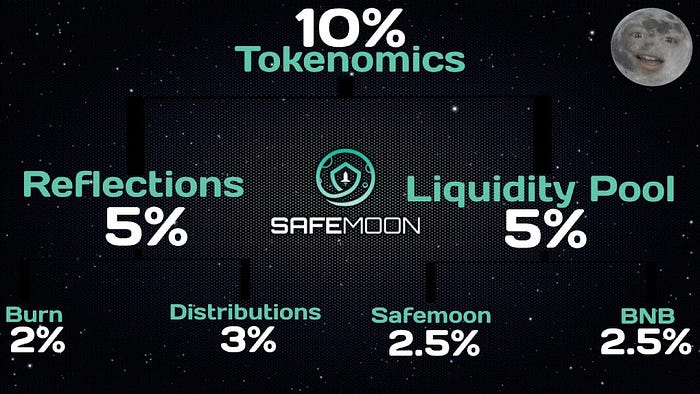

Reflection Tokens

Before we move on to more advanced DeFi concepts, I want to highlight a special token characteristic I see frequently on Binance Smart Chain: transaction tax used towards “reflection” and/or “burn”. The most notable example here is SafeMoon (SAFEMOON), which takes a 10% tax from each transaction split four ways. 3 of the 10% is redistributed to all current holders regardless of if they are staked or not. So the token automatically generates yield when sitting in your wallet, whether you opt-in or not.

Speaking of wallets, Safemoon currently has 2.5M holders and over a $1B market cap, though its only real product is the value generated for early token hodlers who can tolerate wild price fluctuations and the eventual 10% exit fee. The unique tokenomics and marketing of the token itself are the product, rendering it a memecoin like DOGE its little cousin SHIBA INU. Let’s stay away from these for now…

Not all reflection tokens are memecoins. I first saw this tokenomics rule back in April on one of my favorite tokens to talk about: CumRocket (CUMMIES). I say this because CR illustrates a clear application of DeFi, namely the adult content industry.

In fact, Papa Elon agrees and tweeted his endorsement! This mania rocketed the price up to $0.3 for an hour before numerous whales unloaded their tokens and caused a panic sale. Unfortunately it was the middle of the night in the US and I missed my chance to take a very healthy profit, but I woke up that morning with a lot of free tokens redistributed from the transaction tax. So I can personally verify that this reflection is indeed real.

The logic behind the 2.5% burn is that it makes the currency deflationary, thereby ensuring the token retains value over time. Ethereum’s London hard fork will make it a deflationary currency as well. Tokens received from the 2.5% redistribution entirely depends on the trading volume, so it is difficult to quantify with an APY. And remember that you too will have to pay the 5% tax when you eventually sell.

We have covered most of the ways in which you can stake a token to earn rewards for providing value. Diversification reduces exposure, so it behooves you to combine multiple assets and methods into your yield farm.

Now we arrive at the heart of DeFi: Liquidity used as “Money Lego Blocks”. My mother founded a Lego Robotics Institute so I am quite familiar with these famous plastic bricks. This popular metaphor highlights the composability of crypto assets: the ability to stack them together like Legos to build a larger financial structure. Smart contracts enable developers to programmatically organize money and logic to achieve a specific purpose. This section explains popular “composite” yield farming patterns that involve multiple tokens.

Liquidity Mining

If a Dapp/Token starts gaining traction, consumers often want to buy the token with different currency pairs other than say ETH or BNB. For example if a startup provides services for a relatively risk-averse customer segment, they should prioritize supporting as many stablecoin pairs as possible. Or conversely if a platform wanted to capitalize on the surge in popularity of a new coin such as SHIBA INU, they can attract users by supporting swaps from a wide range of crypto assets. Synthetix (SNX) first introduced this model in July 2019 to support trading between ETH and a new “synthetic” asset sETH.

To establish such tradable pairs, DeFi companies incentivize investors to become “Liquidity Providers” and stake their tokens in the platforms Liquidity Pools. This is where Decentralized Exchanges (DEX) comes in. Uniswap, Pancakeswap, 1inch, and more recently Sushiswap are some of the bigger players, but there are probably thousands of DEXs out there.

To understand what DEX’s are not, let’s take a quick look at RobinHood and what happened when everybody decided to buy the same stock on the same day. Around midday on January 28th 2021, RobinHood halted trading on GME, AMC, and other names because the company didn’t have enough collateral in the bank to process the unprecedented volume of trades. Stock transactions may seem instant on mobile apps, but the cash actually takes +2 days to settle before it can be withdrawn into useable currency. So even though a customer may have enough money to deposit and make a trade, Robinhood and all other trading firms are required to use its own deposited funds at a “clearinghouse” to cover risks until trades are settled.

While over-enthusiastic retail investors were trying to join the party and buy GME at an absurd price, there were numerous investors who wanted to sell their GME shares and take profit. But none of these trades happened since RobinHood and other brokerage firms halted trading until the market somewhat stabilized. This seemingly-unfair course of action enraged all retail investors, some seasoned traders, Redditors, US politicians, and many others who lament these glaring issues with our centralized financial instruments and their gateway institutions.

This would never happen on a Decentralized Exchange. Firstly, all trades or ‘swaps’ are settled immediately, and the user always has full custody of their funds. More importantly, the DEX functions as a market that automatically fulfills orders without relying on traditional buyers and sellers. This is achieved using Automated Market Makers (AMMs) which provide 24/7 markets via liquidity pools. If you are interested in learning more about how AMMs works, this article from Gemini explains it nicely. From the perspective of yield farming, just know that AMMs generate the value from providing liquidity between a pair of tokens.

Let’s say you want to provide liquidity to The Graph (GRT), a promising blockchain indexing protocol. In return for supplying a token pair that supports trading between say ETH and GRT , you receive Liquidity Pool (LP) tokens that represent your % share of an ETH-GRT LP. These LP tokens earn you rewards which are generally compounded to the initial position: notice the “Liquidity Provider Fee” on the Uniswap confirmation dialog.

There are some crucial caveats when investing in composite products such as LP tokens, which represent a proportional combination of two cryptocurrencies: the sum of the parts is very different than the whole. There’s a tricky concept called “divergent loss” (more commonly “impermanent” loss which is a misnomer) that must be taken into account when investing in liquidity.

Liquidity pools rebalance to handle transactions and price changes in the underlying assets, so you may not receive the same proportion of tokens or dollar value that you deposited. They follow the formula x * y = k, where x and y represents the respective token balance of a pairing and k is a constant. Any trade changes the balance of a liquidity pool: this allows “arbitragers” to rebalance assets across exchanges, so over time the ratio of tokens in the pool follows the market.

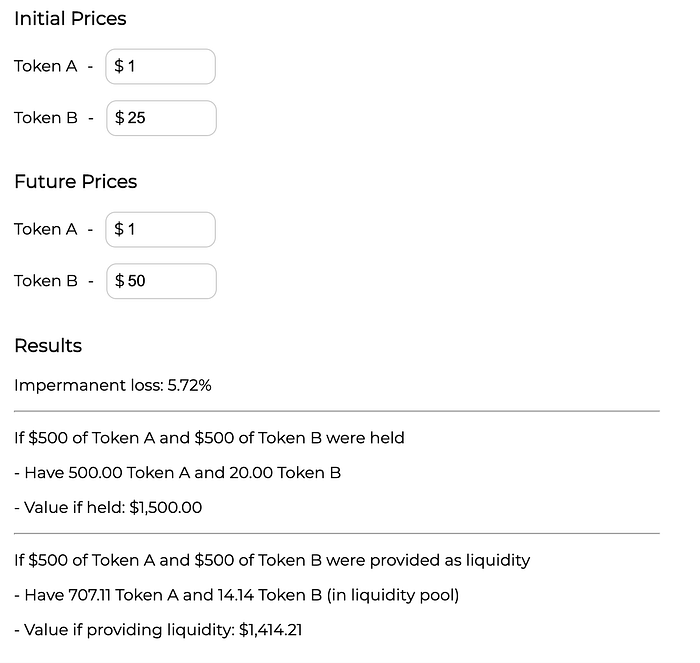

If you haven’t seen any of this and are totally lost, don’t worry: we will focus on functionally illustrating how the underlying tokens price movements impact a liquidity position. Say you stake funds to a USDC-LINK LP, and hypothetically later this year Chainlink (LINK, the original blockchain oracle which “connects smart contracts to the outside world”) doubles from $25 back to its May highs of $50. The rebalancing of this liquidity pool will cause you to miss out on 5.72% of the profits, which is the “divergent” or not-so-”impermanent” loss.

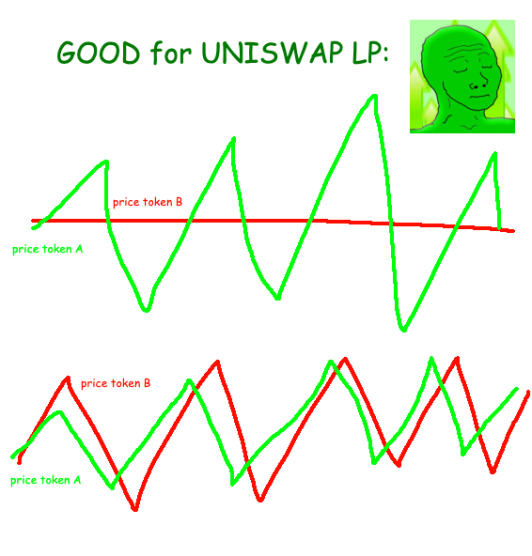

Conversely a sharp decrease in the underlying assets is compounded. For instance a 37.5% value loss sinks to -50% as a liquidity position. Here’s a humorous graphic from Twitter user Fiskiantes:

To qualify the above diagram, opposite-direction price movements are not necessarily disastrous for the LP value. I think the reason the for the graphic is that you would miss out on most of the profits from token B, which as many investors know can feel worse than the losses from token A. So providing liquidity between two varying assets (ie. no stablecoins) is a risky game. I highly recommend plugging in values to a calculator before attempting such a stunt.

Relatively proportional movement in both assets is optimal, since the LP ratio (x * y = k) stays roughly the same. We can sum it up with the following:

Liquidity Providing is a seminal innovation in Defi, and has quickly become a hot way to earn income while supporting a decentralized market. As I said at the start: Yield Farming is all about growing both your position and the larger DeFi ecosystem, not solely betting on price movements. That being said, you should be cognizant of how of price changes impact liquidity value.

Uniswap v3 Concentrated Liquidity

Since Uniswap is the largest DEX with consistent daily trading volume of around $1B, their latest release deserves a designated section. The v3 upgrade is said to be a game changer because it allows LP’s to “provide liquidity with up to 4000x capital efficiency relative to Uniswap v2, earning higher returns on their capital”. See Uniswap’s video explanation here.

The core concept remains the same, but you can now set a price range between which you want your liquidity to be concentrated. Uniswap v2 liquidity was always distributed evenly between $0 and $Infinity for all token pairs, so most liquidity was never actually utilized. Especially for stablecoins where the price varies little over 0.99 and 1.01, concentrating liquidity around $1 to activate the previously-unused 99.5% of the pool seems only logical.

The reason the game changes is because users are now responsible for managing their own liquidity price parameters: if I want, I can pool stablecoin pairs like USDC-MIM (“Magic Internet Money”, my favorite stablecoin) between $0.1–$0.8 and never have my liquidity used. This used to happen behind the scenes on Uniswap, and still does on most DEXs, so previously they just rewarded everyone equally. But now this liquidity position would not yield me any rewards since it would never be ‘activated’.

Uniswap v3 LP tokens represent “non-fungible liquidity”, or unique LP tokens that contain data about the users desired price range. This is a massive technical achievement that enables a wide range of new liquidity products. But the casual investor must be extra careful getting into concentrated liquidity mining. Most people (including myself) are probably better off using a yield manager or “aggregator” like Harvest.finance with predefined price ranges and highly appealing rewards.

Yield Aggregators

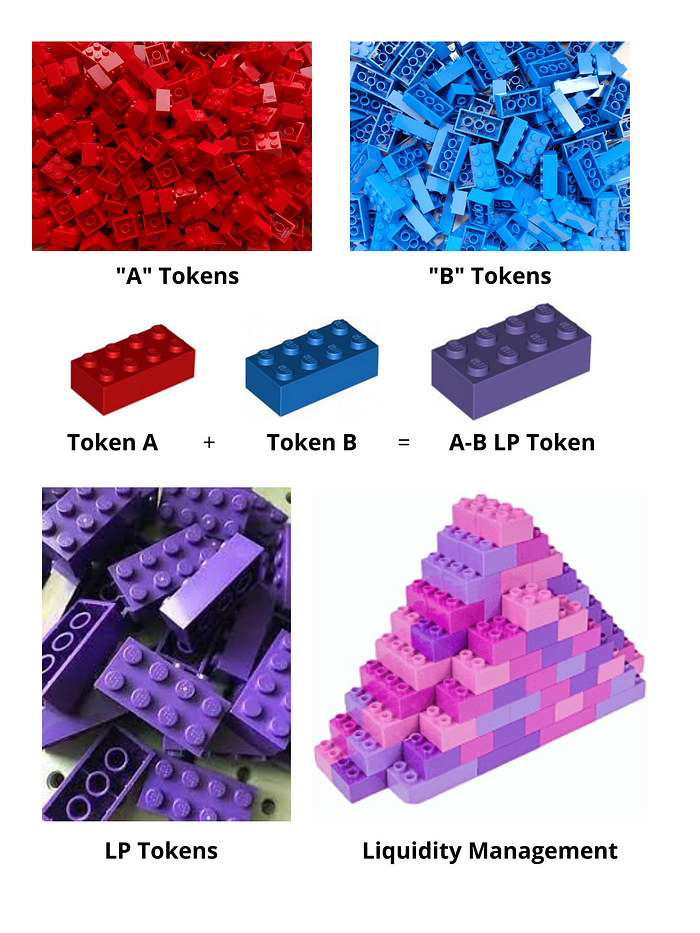

Let’s do a quick recap of LP using Legos

- Buy piles of red and blue bricks and dump them on a table.

- Connect a pair of red and blue bricks to create a special purple brick. Repeat for all red and blue brick pairs.

- End up with a table full of purple bricks without knowing where to put them.

Yield Aggregators (or “yield maximizers” as coined by Pickle.finance) actively manage investors’ liquidity positions by leveraging different DeFi protocols and strategies to maximize the liquidity’s activation and associated rewards. Using the Lego analogy, they stack purple bricks pooled from multiple investors, and rearrange bricks to optimize their contribution at any given time. This movement of LP assets is technically the definition of yield farming as a verb, but I think of farming in broader terms of actively managing yield-bearing crypto assets, including single-token methods described earlier.

These liquidity management platforms are startups like any other DeFi platform, so in return for contributing to the TVL users are rewarded with free tokens. Harvest.finance’s APYs are hard to beat, especially for tokens like ETH and USDC that have widespread investor confidence.

Harvest.finance (FARM) was only recently listed on Coinbase for trading, and most yield management platforms don’t have high enough TVL to inspire widespread confidence just yet. So keep an eye out for creative startups and bookmark this useful list by DefiPrime.

Sustainable Farming

Things get really interesting when we start combining different reward mechanisms to create a self-sustaining yield farm.

We have a couple building blocks in place now:

- Single-token deposits: to facilitate lending or platform functions

- Two-asset Liquidity Pool token: to facilitate trading

- Staked LP tokens: to aggregate and maximize liquidity usage

As pictured earlier, Harvest.finance rewards users with Uniswap (UNI) + native FARM tokens for staking ETH-USDC LP. So we could periodically harvest these rewards and put them back into another part of our investment portfolio. For example, we could deposit the UNI rewards into Aave and stake FARM on Harvest, or grow a new UNI-FARM LP position. Platforms incentivize staking positions with a variety of tokens, and we must decide how best to use these rewards. What if we put them into another farm, and put the output from that farm into yet another farm, and so on…?

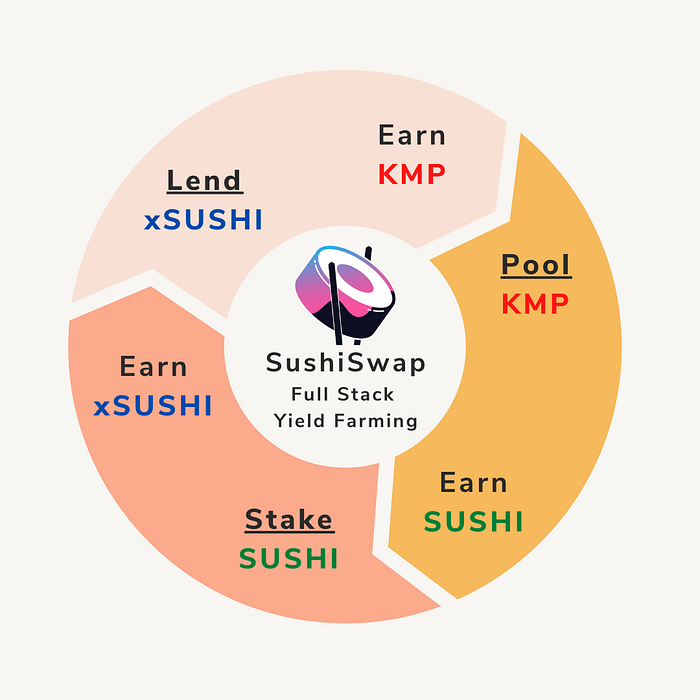

The only “full-stack” yield platform I have seen thus far is SushiSwap. They explain the process in their docs, but here is a simple infographic that encapsulates it:

This is essentially a circular orchestration of yield farms where the output of any given Farm is the input of another Farm, forming a closed-loop system. And though such processes are currently manual, I imagine these workflows will soon be automateable. I am supremely excited about the future of yield farming, and the innovation it will inspire along the way!

This final section covers a very risky and advanced farming method where you can easily lose all the money you put in. Leveraged/Margin trading is undoubtably dangerous, definitely a “don’t try this at home” for most investors. And don’t think crypto is exempt from the law — the IRS will most certainly come after you for defaulting on loans and withholding cap-gains taxes.

Leveraged Farming

Let’s go back to Aave and imagine we deposited 2 ETH at $1,800 each on July 20, 2021. Our $3,600 collateral in ETH allows us to borrow up to 80% of this, but let’s be safe and borrow $2,000 of USDC at a roughly 3.5% variable APY. So in a years time, we would owe Aave about $2,070 and still have 2 ETH in the bank.

One strategy from here is to execute a simple “carry trade” that involves depositing the borrowed USDC into another stablecoin/platform combination that provides a higher rate of return. If you trust the platform, you could put this USDC into Nexo to earn 12% interest and pocket the difference, but this isn’t really farming.

Back to our Aave funds: at the time of writing ETH is at about $2,700, a 50% gain from our July 20th deposit (that was quick!). Our 2 ETH has appreciated with an $1,800 profit which pays off most of the USDC loan, in a much shorter time frame than the advertised annual rate. This is the basic principle behind leverage: borrowing a fixed amount against collateral you believe will appreciate.

Now say you want to yield farm in a certain LP, but don’t want to waste a portion of your funds on non-appreciating USDC. You could borrow this USDC against the other token in the pair. As promised, we finally return to SolFarm:

In one action: users can borrow USDC against the current value of RAY, and pool the combined tokens as a leveraged, non-fungible, staked RAY-USDC liquidity position.

Assuming the price of RAY goes up, the equity value increases and starts paying off the debt value. Just as in the Aave example: if the value (price * quantity) of our RAY position doubles, our loan is automatically paid off. It is easier to understand by actually seeing a sample position. Notice the bonus TULIP tokens (recently harvested) on the bottom-left.

But on the far right there is a 36% Kill Buffer, which by its name can’t be good. Let me emphasize this again: leveraged or margin trading is extremely risky! If the price of RAY drops and the Loan-to-Value (Debt) ratio breaches the 85% threshold, the entire position is lost. On the other hand, $32.70 or 1.9% growth in less than a week is quite compelling; and one could use the TULIP rewards to pay off the debt, or send it to another yield farm…

Concluding Remarks

If you’ve made it this far, you must either be a DeFi enthusiast or a clever person who sees no reason to not earn yield. Hopefully at least one of the ten or so ways I outlined above fits your risk profile and tech skills. And if not, maybe we can try a different approach: I have seen a couple emerging platforms such as Gourmet Galaxy that offer gamified art-centric experiences.

My favorite aspect of Yield farming is that it’s more organic than traditional investing, since gains are contingent on supporting the larger ecosystem rather than betting on how other farmers crops may turn out. “Providing Liquidity”, however, implies that we give up liquidity of our own. So if the need arises, how would one convert these complex, composite, compounding, crypto assets back to cold hard cash?

Most of these investment options are not for the faint hearted: it can be a long, wasteful, gas-intensive journey for this money to transform back into fiat. I would have to take the following steps to go from a staked liquidity position to useable USD.

- Harvest currently accrued rewards

- Unstake liquidity positions

- Swap LP tokens to underlying assets

- Swap assets to ETH network (if on BNB, SOL, MATIC, etc.)

- Swap ETH (ERC20) assets to USDC

- Send USDC to Coinbase account

- Convert USDC to USD on Coinbase

- Withdraw to Chase bank account

- Wait a few days…

I am excited to try out the Coinbase and Gemini credit cards, and am particularly interested in the interaction with USDC. This bridge between the centralized and decentralized financial worlds is crucial to the widespread adoption of DeFi. One day, I hope to tip an NYC subway musician in tokens.

To wrap things up, the following list contains all the crypto-crops I have cultivated in my yield farm. I close positions that feel are suspicious or overly risky, rebalance funds periodically within the same blockchain, and closely follow price alerts from CoinStats, Blockfolio, Gemini and others. I only started farming in earnest around May 2021, so this list will keep growing!

- Solana Beach Validator node SOL delegation

- Polygon Stakin node MATIC delegation

- Aave deposits of ETH, UNI, USDC

- PancakeSwap CAKE AutoCompound staking

- Harvest.finance FARM staking

- SushiSwap xSUSHI membership

- Dodo vDODO membership

- CumRocket CUMMIES reflection tax

- Balancer WETH, WMATIC, MTA pool

- DeFiPulse ETH-DPI LP for INDEX

- Abracadabra.money MIM-ETH LP for SPELL

- Harvest.finance Uniswap v3 ETH-USDC LP for UNI + FARM

- SolFarm Staked LP positions

- SolFarm Leveraged Farming RAY + USDC position

- Origin Token OGN fixed 90-day contract (inactive)

- Nexo interest on USDC (inactive)

- TrustWallet BNB (inactive)

-Written by Aditya Nirvaan Ranganathan